SEC Climate-Related Disclosure Proposal: Charting the Path Forward

Executive Summary:

- The SEC has issued a proposal requiring companies to disclose information about corporations' climate change risks within their filings.

- This proposal includes new requirements for qualitative and quantitative disclosures, attestations, and audit reporting requirements for Scope 1 and 2 Greenhouse Gas emissions.

- The SEC’s goal in creating this new proposal is to drive greater transparency from registrants to protect investors and solidify climate-related disclosures as required reporting.

On March 21, 2022, the U.S. Securities and Exchange Commission (SEC) issued a proposed rule that would require registrants to include climate-related disclosures within registration statements and annual reports (including Form 10-K). According to SEC Chair Gary Gensler, the rule is intended to promote transparency and protect investors, providing them with “consistent, comparable, and useful information for making their investment decisions.”

With a 3-1 passing vote, the SEC’s formal proposal has now opened a public comment period which seeks responses from the impacted companies, accounting firms, and the public at large (note the comment period will end on May 20, 2022, or 30 days following the publication in the Federal Register, whichever is later).

While updates to the proposed regulations are likely to follow the closure of the comment period, it is already evident that mandatory climate-related disclosures are close. Further, given the complexity of the proposal, it is apparent that registrants will experience increased costs driven by new governance and reporting requirements - and these costs could extend through the registrant’s entire value chain (including upstream suppliers and downstream customers).

MGO’s Environmental, Social and Governance (ESG) practice has inspected the proposed rules and provides a summary and contextual overview in the following paragraphs.

Note: The complete, 506-page SEC proposal is viewable here, while a 3-page summary fact sheet is viewable here.

SEC proposed climate disclosure requirements

Through its independent research of 6,644 annual filings, the SEC found that many companies were already disclosing both qualitative and quantitative metrics related to climate change (i.e., on a voluntary basis). Additionally, the SEC found that a subset of those companies was doing so in line with two of the most common frameworks and standards:

- Task Force on Climate-Related Financial Disclosures (TCFD) - The framework primarily used by companies that make qualitative, climate-related disclosures around governance, strategy, and risk management as well as certain quantitative disclosures (i.e., the metrics and targets used by a company to measure and assess climate risks, opportunities, and targets)

- Greenhouse Gas Protocol - The standardized framework used by most organizations to inventory, calculate, and manage greenhouse gas (GHG) emissions (i.e., the quantitative disclosures commonly referred to as Scope 1, Scope 2, and Scope 3 GHG emissions)

At the highest level, the proposal’s new disclosure requirements include:

- New qualitative disclosures (under Regulation S-K) in a separate, captioned section of the annual filing, including but not limited to descriptions of:

- The governance of climate-related risks (e.g., board and management oversight)

- Material climate-related impacts on strategy, business model, and outlook

- Approaches to climate-related risk management

- GHG emissions metrics (e.g., Scope 1, Scope 2, and potentially Scope 3 emissions)

- Climate-related targets and goals, if any (e.g., net-zero commitments)

- Usage of an internal carbon price and how this price was determined

- New quantitative disclosures (under Regulation S-X) included as a note within the audited financial statements, including:

- Disaggregated information about the climate-related impacts, events, and transition activities to existing financial statement line items (FSLIs) above a certain threshold (e.g., increases to reserves, impairment charges, expenditures specific to transition activities, etc.)

- Incremental attestation and audit requirements

- Scope 1 and Scope 2 GHG emissions disclosures (under Regulation S-K) would be subject to an attestation requirement; however, the disclosures would initially be subject to an audit under the limited assurance standard and followed by an audit under the reasonable assurance standard two years later

- Climate-related impacts, events, transition activities, etc. to existing FSLIs would be subject to existing audit requirements (i.e., consistent with procedures performed over historical financial statement footnotes, including internal controls over financial reporting [or ICFR])

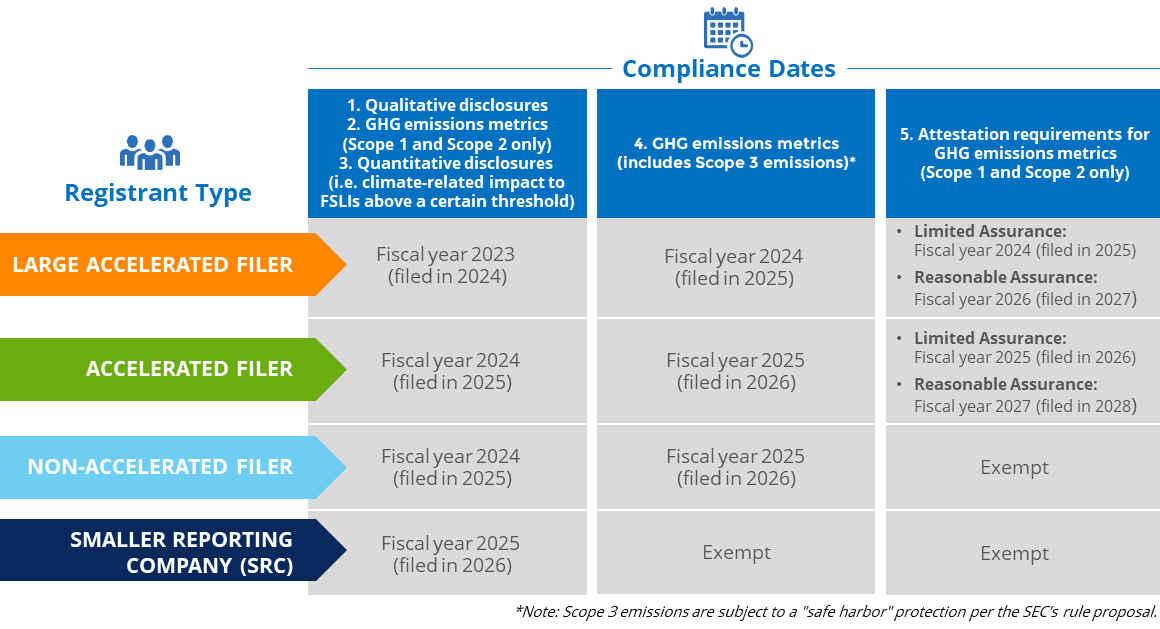

When would the proposed climate-disclosure updates go into effect?

Under the proposed rule (which is subject to change after the comment period), domestic and foreign registrants would be required to adhere to the following phase-in timelines:

MGO's perspective

Through our experience to date, and corroborated through the review of the SEC’s analysis of 6,644 annual filings (refer to pages 311-320 of the 506 page proposal for the analysis), many registrants across all industries are already voluntarily disclosing climate-related information. However, for the companies that have not yet moved to establish climate-related governance, evaluate their existing business strategies, analyze the emerging risks, or inventory the data required for climate-related metrics, the compliance effort is expected to be considerable.

In the end, the SEC’s goal with the proposed rule appears to be two-fold:

- The first is to drive transparency from registrants to protect investors. As many issuers already disclose climate-related information voluntarily, standardizing the requirements will provide more comparable information while reducing compliance costs in the long run

- The second is a recognition that climate-related disclosures are not only here to stay but set to grow in importance in the coming decades. Given that anticipated growth, the SEC’s proposal will ensure the US regulatory environment is able to keep pace — especially with its international counterparts

Regardless of your company’s current maturity as it relates to climate governance, strategy, risk assessment, and disclosure, the time to act is now. Rule proposals of this scale and complexity from the SEC are infrequent, and with international regulators looking to adopt their own sustainability disclosure requirements (see the IFRS Foundation’s Sustainability Disclosure Standards draft released on March 31, 2022), we expect the path to compliance will be long and ambiguous for many.

Lastly, while the proposal is intended for public registrants, we believe that private companies also need to begin to mobilize. As an example, if a private company operates as a vendor or supplier for a Large Accelerated filer with Scope 3 emission reporting ambitions, the privately held vendor or supplier can expect that Large Accelerated filer to request timely and quality Scope 1 and/or Scope 2 GHG data to serve as an input into the filer’s Scope 3 calculation (inclusive of questions around the completeness and accuracy of data).

Questions to consider about the SEC’s proposed ESG ruling

- Who is responsible for governance and oversight (at both the board and management level) of climate-related risks and opportunities?

- Which climate-related frameworks and/or standards has the company considered adopting or are already following for existing disclosures?

- Are existing qualitative and quantitative climate-related disclosures robust (i.e., considered investor-grade)?

- Are there sufficient processes and controls in place to ensure climate-related disclosures are complete, accurate, and timely?

- Is a communication plan in place to make employees aware of climate-related risks, opportunities, commitments, and progress?

- Does the board understand why ESG-related information (which is broader than the information in the climate-disclosure proposal) is important to investors and other stakeholders?

Regardless of your ESG program’s maturity, the definition of value is evolving, and organizations that evolve with it are primed for long-term success.

For insights tailored to your company and industry, schedule a conversation with our ESG team today.