Executive summary

- The Supreme Court of Washington State issued a landmark ruling maintaining the constitutionality of the state’s capital gains tax (CGT) by determining that it’s an excise tax, or a tax on a good or service (and not a property tax).

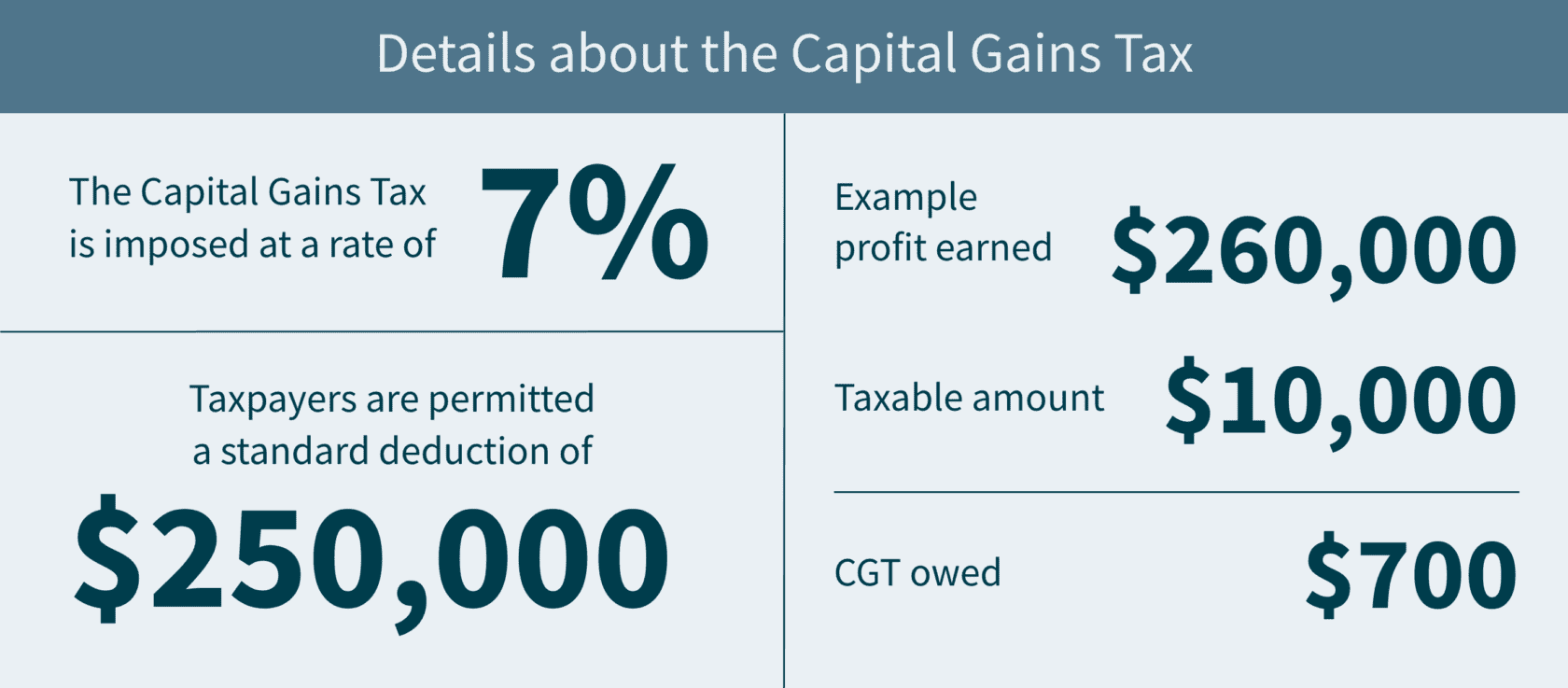

- It’s imposed at a rate of 7% and taxpayers can claim a standard deduction of $250,000.

- There are other deductions, like long-term gains from the sales of qualified family-owned small businesses and charitable contributions of more than $250,000.

- You may be able to apply a tax credit.

On March 24, 2023, the Supreme Court of Washington State (SCOWA) ruled 7-2 to uphold the constitutionality of the state’s controversial capital gains tax. Thus, by the April 18, 2023, deadline, Washington residents recognizing capital gains income (and nonresidents engaged in transactions occurring within the state) in 2022 will have to calculate this new tax and pay accordingly.

Our State and Local Tax team breaks down what you need to know about this divisive tax with an impending deadline.

The details about CGT

The CGT was created when Washington enacted Senate Bill 5096 in April 2021 with the intention of having the excise tax proceeds — projected to be nearly $415 million — fund the state’s early education and childcare programs. Charged on long-term Washington-allocated capital gains, the CGT is imposed at a rate of 7% of an individual’s federal capital gain from a sale or exchange of long-term investments that exceed $250,000. This includes stocks, bonds, businesses, and other assets.

The controversy of CGT

This bill has generated controversy since its inception — mostly because it is categorized as an excise tax and not an income tax (Washington is one of nine states that doesn’t have income tax due to limitations in the state constitution on the state government assessing a tax on “property”). As a reminder, an excise tax is a legislated tax on the sale of specific services, activities, or goods.

In March 2022, the Douglas County Superior Court in Washington deemed the CGT unconstitutional as an impermissible income tax that is only masquerading as an excise tax. The Court defined gains as income, and therefore property under the Washington Constitution, that the state impermissibly taxed at a non-uniform rate (i.e., the tax doesn’t apply to every resident equally, but only those whose profits exceed the $250,000 threshold). In the past, Washington’s Supreme Court has considered income as property — and property must be taxed at a flat rate.

Since state revenue relies on sales and business taxes, taxpayers who earn the least will end up paying a higher share of their income in tax. This notion has split public opinion. Community groups and labor unions believe the tax is not just legal, it’s necessary because of its capability to create a more equitable tax system. But organizations with business interests in mind find it to be bad public policy in addition to violating the constitution.

However, the Washington Supreme Court ruled to uphold the tax, agreeing it is constitutional as an excise tax — “levied on the sale or exchange of capital assets, not on capital assets or gains themselves.” In other words, the Court reasoned that the tax is tied not to the person’s ownership interest in the property (which would be unconstitutional), but on the transaction itself.

Calculating your tax base

Adjusted capital gains

As mentioned, the new tax is imposed on your adjusted capital gains allocated to Washington, minus allowable deductions and exemptions. First, it starts with your federal net long-term capital gain for the tax year. It’s then adjusted by adding back long-term capital losses from sales or exchanges that are exempt or not allocated to the state. Finally, you subtract your long-term capital gains from sales or exchanges that are exempt or not allocated to the state.

Deductions

There are several deductions allowed against adjusted capital gains. Individual taxpayers are permitted a $250,000 standard deduction in calculating the CGT. But married or state-registered domestic partners that file a single federal tax return collectively have only a single $250,000 deduction. For example, if you earned $260,000 in profit from selling bonds in the past year, only $10,000 would be taxed, and the CGT owed would be $700. And if you and your husband together earned $260,000 from selling bonds, you wouldn’t get to “double” the standard deduction – you'd have the same tax bill.

Additional deductions include long-term gains from the sales of qualified family-owned small businesses, and charitable contributions. Associated regulations do treat the sale or transfer of an interest in a “qualified family-owned small business” as a separate deduction from the charitable deduction. (Note that the “qualified family-owned small business” is not the same as the federal Qualified Small Business Stock (QSBS) tax exclusion — there are separate requirements). To receive the charitable deduction, you would need to contribute over $250,000, not exceeding a deduction of $100,000 in total. Consequently, if you donate $350,000, you’ll receive the maximum deduction.

Exemptions

Certain long-term capital gains and losses from sales of capital assets are not subject to the tax. These exempt items include sales or exchanges of the following types of assets:

- Livestock;

- Timber;

- Real estate, and land structures; and

- Capital assets held in IRAs, 401(k) plans, and other qualified retirement plans

Allocating your capital gains and losses

If you were living in Washington at the time of a sale or exchange of intangibles (e.g., stocks, bonds, etc.), related long-term capital gains and losses are allocated to Washington.

In addition, gains or losses from the sale or exchange of other (tangible) personal property is allocated to Washington if:

- The property was in Washington at any time during the tax year when the sale/exchange occurred,

- You were a Washington resident at the time of the sale/exchange, and

- You were “not subject to the payment of an income tax or excise tax legally imposed” by another jurisdiction* on that long-term capital gain or loss.

* Jurisdiction is defined to include not only U.S. states, political subdivisions, territories, and possessions, but also foreign countries and political subdivisions of foreign countries.

Good news: a tax credit is available

If you’re interested in applying a tax credit against this new tax, you might be able to. Any Washington capital gains tax can qualify as a credit against the Washington business and occupation (B&O) tax — given that the B&O tax includes the gain from a transaction subject to capital gains tax (because it applies to ALL gross receipts regardless of character).

In addition, a credit can be applied for an income or excise tax legally imposed by another jurisdiction on capital gains “derived from capital assets within the other taxing jurisdiction to the extent such capital gains are included in the taxpayer’s Washington capital gains.”

Filing your returns

Remember, a Washington capital gains tax return is required only if tax is owed — and it must be filed on or before the due date of your federal income tax return, including extensions. But the payment of the tax is required BY the original due date of your federal income tax return, NOT including extensions. Any filing and payments must be done online using the MyDOR portal by April 18, 2023, for most taxpayers.

How MGO can help

Keep in mind that while this tax will more than likely impact Washington residents the most, if you are a nonresident whose capital gains from the sales and exchanges of your tangible personal property is allocated to Washington, you could be affected too. Accordingly, anyone with a large gain event (other than the sale of real property) during 2022 or later years, should consider whether this tax may affect them.

MGO’s State and Local Tax team can help you prepare and file this return and manage any of the other surprises that can occur in state and local tax. Contact us if you have additional questions about how the capital gains tax impacts your finances, or if you’re interested in additional strategies to boost your tax efficiency.