New High-Road Cannabis Tax Credit (HRCTC) for California Retailers and Microbusinesses Worth up to $250k Annually

Executive summary

- California now has a new tax credit called the High-Road Cannabis Tax Credit (HRCTC) available for eligible cannabis retailers and microbusinesses.

- The credit is available for tax years starting after January 1, 2023, through December 31, 2027, and can be applied against current year (and future) income taxes.

- To claim it, you must make a “tentative credit reservation.”

- Expenditures that qualify include wages for full-time employees; safety-related equipment, training, and services; and workforce development and safety.

While the cannabis industry in California has been struggling on many levels, tax credit relief has come in the form of excise tax changes for distributors and has now arrived for retailers. The High-Road Cannabis Tax Credit is a new tax credit from the California Franchise Tax Board (FTB) available for cannabis retailers or microbusinesses for taxable years beginning January 1, 2023, through December 31, 2027. In order to capitalize on this opportunity, eligible calendar-year taxpayers must make a tentative credit reservation during the month of July to claim the credit on their 2023 CA income tax return.

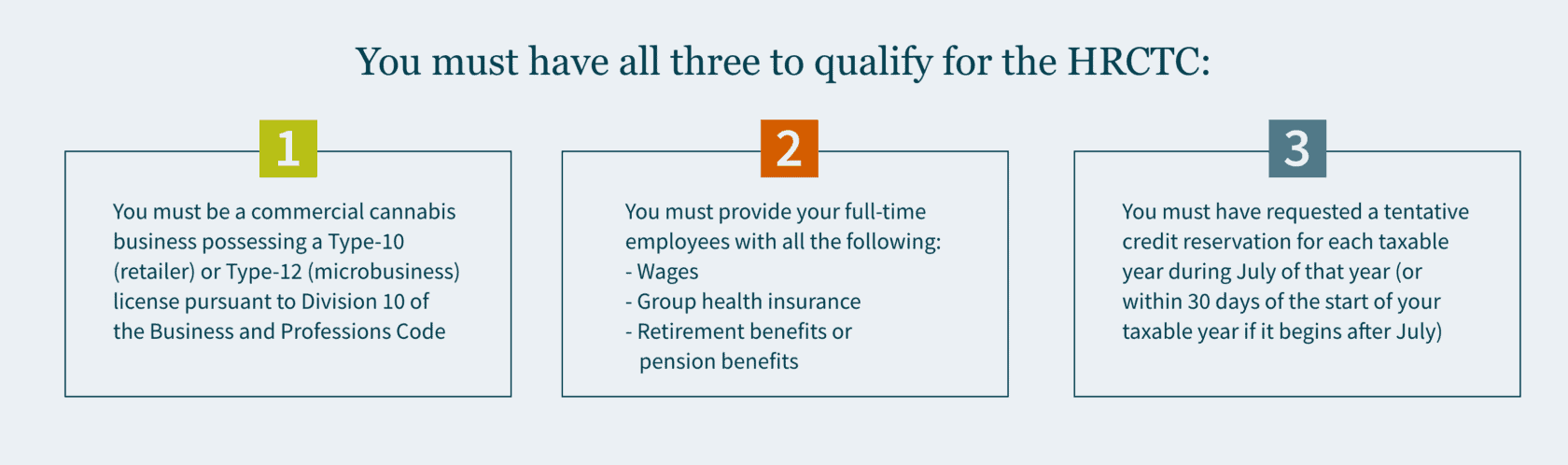

Who qualifies for the HRCTC

To be eligible, you would need to meet three basic requirements.

Which expenditures qualify for the HRCTC

There are several types of expenditures eligible for the credit with specific parameters that you would need to meet to qualify for them. Qualified expenditures are amounts that you have paid or incurred for any of the following expenses.

Wages for full-time employees

Not every employee has to meet these requirements — but for those that do, their wages count as a qualified expenditure. First, full-time employees must be paid for no less than an average of 35 hours per week — or they must be a salaried employee paid compensation for full-time employment.

In addition, full-time employees must be paid no less than 150% ($23.25) but no more than 350% ($54.25) of the state minimum wage. To meet the 150% minimum wage requirement, you may include the following employee benefits in qualified wages: group health insurance, childcare support, employer contributions to employer-provided retirement plans, or contributions to employer-provided pension benefits. But if you pay employees wages that surpass more than 350% of the state minimum wage, those wages are not considered a qualified expenditure.

Safety-related equipment, training, and services

Expenditures related to safety, training, and providing services can also qualify if they meet the following criteria:

- Equipment primarily used by the employees of the cannabis licensee to ensure personal and occupational safety, or the safety of the business’s customers.

- Training for nonmanagement employees on workplace hazards. (This includes safety audits, security guards, security cameras, and fire risk mitigation.)

Workforce development and safety

Qualified training for your employees includes:

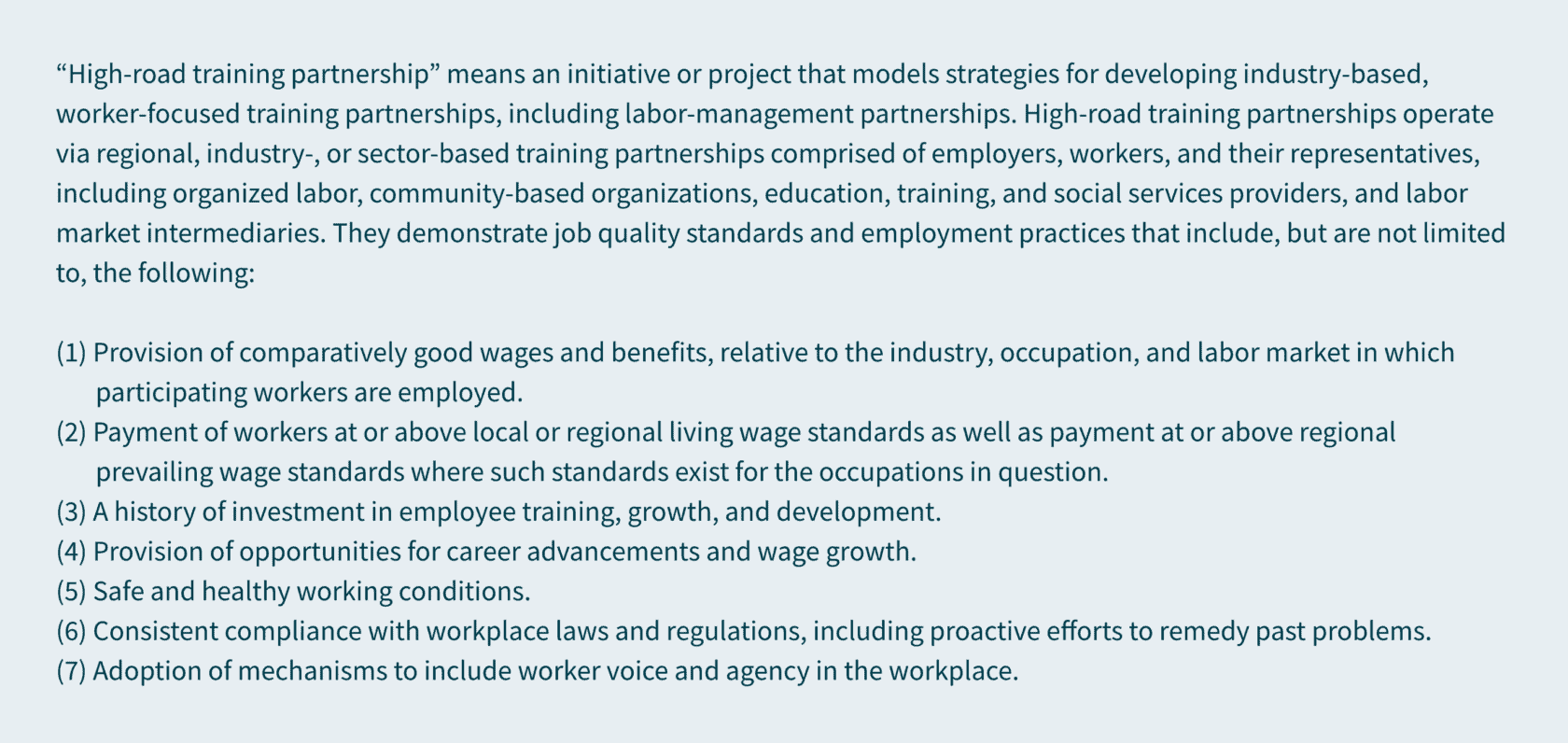

- Joint labor management training programs

- Membership in a joint apprenticeship training committee registered by the Division of Apprentice Standards, and a state-recognized “high-road training partnership” (as defined in Section 14005 of the Unemployment Insurance Code).

Available credit

The amount of available credit is equal to 25% of qualified expenditures. The aggregate credit that can be claimed by each taxpayer (as determined on a combined reporting basis) is a maximum of $250,000 per year. Any unused credit can be carried over to the following eight taxable years. Availability is limited as the total cumulative amount of HRCTC available to all taxpayers is $20 million.

To claim the HRCTC on your California tax return, you must reduce any deduction or credit otherwise allowed for any qualified expenditure by the amount of the HRCTC allowed.

How do I make a tentative credit reservation — and when?

You must make a tentative credit reservation (TCR) with the FTB to claim the credit. This reservation must be made online and once you’ve done so, you’ll receive an immediate confirmation. FTB currently reports that the system will be up and running by July 1, 2023, but you can start preparing now.

How we can help

The HRCTC is a valuable tax credit opportunity for any commercial cannabis business operating in California. Determining if you qualify and calculating how much you can save could be complex. Our extensive experience in cannabis, cannabis tax, and state and local tax enables us to help you take advantage of this tax credit so you can stay focused on thriving in this ever-growing, culture-shaping industry.

Reach out to MGO’s State and Local Tax team to find out whether you qualify for this tax credit opportunity and determine how much you could potentially save.