Key Takeaways:

- Chicago now taxes certain social media businesses based on monthly Chicago consumer data collected above a 100,000-user threshold.

- The personal property lease transaction tax rate increased to 15%, affecting software, SaaS, and cloud-based services used in Chicago.

- Businesses may need to reassess consumer sourcing, data analysis, and SALT compliance processes to address expanded city tax exposure.

—

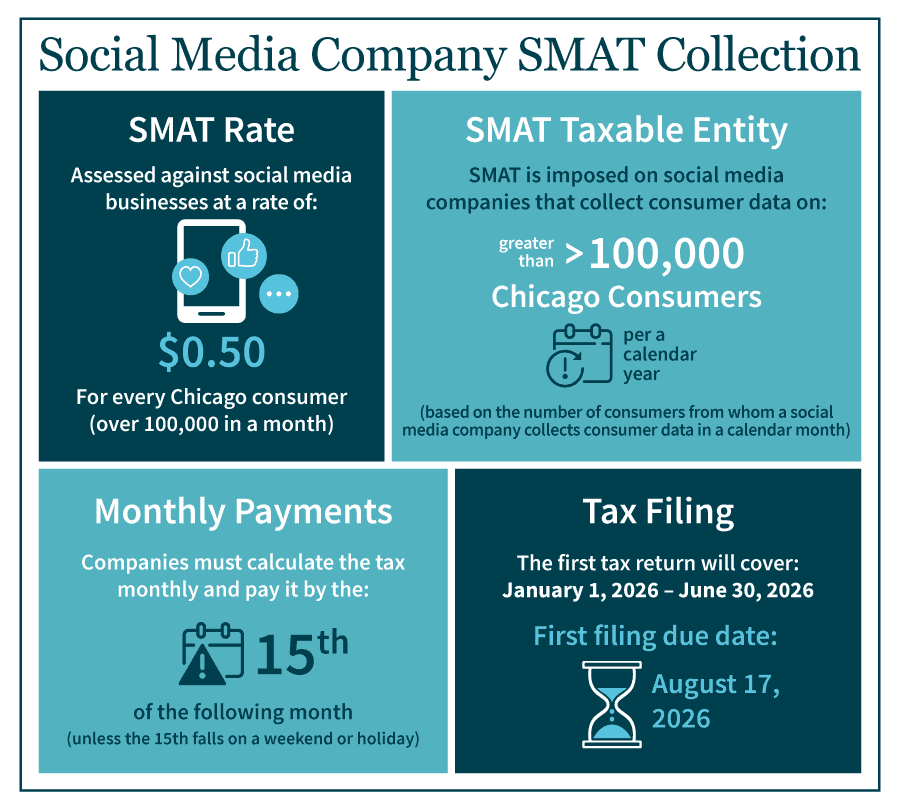

New Social Media Amusement Tax (SMAT)

Chicago is the first U.S. city to impose a tax specifically targeting certain social media businesses. The SMAT applies to for-profit social media companies that collect consumer data from more than 100,000 Chicago consumers during a calendar year.

The tax is calculated monthly and assessed at $0.50 per Chicago consumer per month for each consumer above the 100,000-user threshold.

Filing and Payment Requirements

- Tax calculation: Monthly

- Payment due date: 15th day of the following month (adjusted for weekends and holidays)

- First payment due: February 16, 2026 (for January 2026 activity)

- Tax return filing: Annual

- First return period: January 1, 2026 – June 30, 2026

- First return due: August 17, 2026

Personal Property Lease Transaction Tax Increase

Effective January 1, 2026, Chicago increased the Personal Property Lease Transaction Tax rate from 11% to 15%.

The tax applies to the lease of personal property used in Chicago, including:

- Tangible personal property

- Software

- Software as a Service (SaaS)

- Cloud-based services

This increase may affect businesses that rely on subscription-based technology, digital platforms, and cloud infrastructure.

What These Changes May Mean for Businesses

Chicago’s recent tax changes reflect a broader trend among cities seeking to capture revenue from digital activity and technology-enabled services. As these rules take shape, businesses with operations or customers in Chicago may find it helpful to revisit how consumer data is sourced, how leased technology is classified, and how local tax requirements align with existing compliance processes.

MGO follows these developments closely and works with organizations as they consider the practical implications of evolving city and state tax policies. Taking a coordinated view of local changes alongside broader SALT considerations can support clearer visibility into compliance requirements and help businesses stay aligned as tax frameworks continue to evolve.

Key Definitions and Technical Clarifications

Amusement

Engagement with media content delivered through social media for the primary purpose of entertainment or enjoyment.

Social Media Business

A for-profit entity that provides individuals access to social media and collects, maintains, uses, processes, sells, or shares consumer data other than basic consumer contact information.

The ordinance excludes:

- News organizations

- Internet search and service providers

- Email services

- Online video games

- Streaming services with non-user-generated content

- Communication services

- Advertising networks delivering solely commercial content

- Telecommunications carriers

- Broadband services

- Cloud computing services

- Technical support services

Intercompany data transfers are excluded, as entities within a controlled corporate group are treated as a single taxpayer.

Chicago Consumer Standard

A Chicago consumer is defined as a Chicago resident who uses social media within the city and whose consumer data is collected, regardless of whether the individual pays for access.

Social media businesses are responsible for determining consumer location. A rebuttable presumption applies when available data reflects a Chicago home address, mailing address, IP address, or primary usage location associated with Chicago.

How MGO Can Help

Chicago’s new Social Media Amusement Tax and increased Personal Property Lease Transaction Tax introduce nuanced sourcing, classification, and compliance considerations that may require careful technical analysis. MGO’s Manufacturing and Distribution team works with digital, technology, and multi-state business to evaluate consumer location methodologies, assess exposure under local tax regimes, review SaaS and cloud-based leash classifications, and align reporting processes with evolving city-level requirements. By integrating these changes into a broader SALT strategy, organizations can strengthen compliance visibility, mitigate their risk, and make informed operational decisions as municipal tax frameworks continue to expand. Contact us to learn more.